Most Australian homeowners are sitting on a loan they set up years ago, quietly paying thousands more than they need to simply because switching feels complicated. The truth is, your financial situation has probably changed since you first signed those papers, and your loan structure should change with it. Understanding when refinancing makes sense can put serious money back in your pocket, and with the right guidance from experienced brokers like Credific Finance, the process is far simpler than most people think.

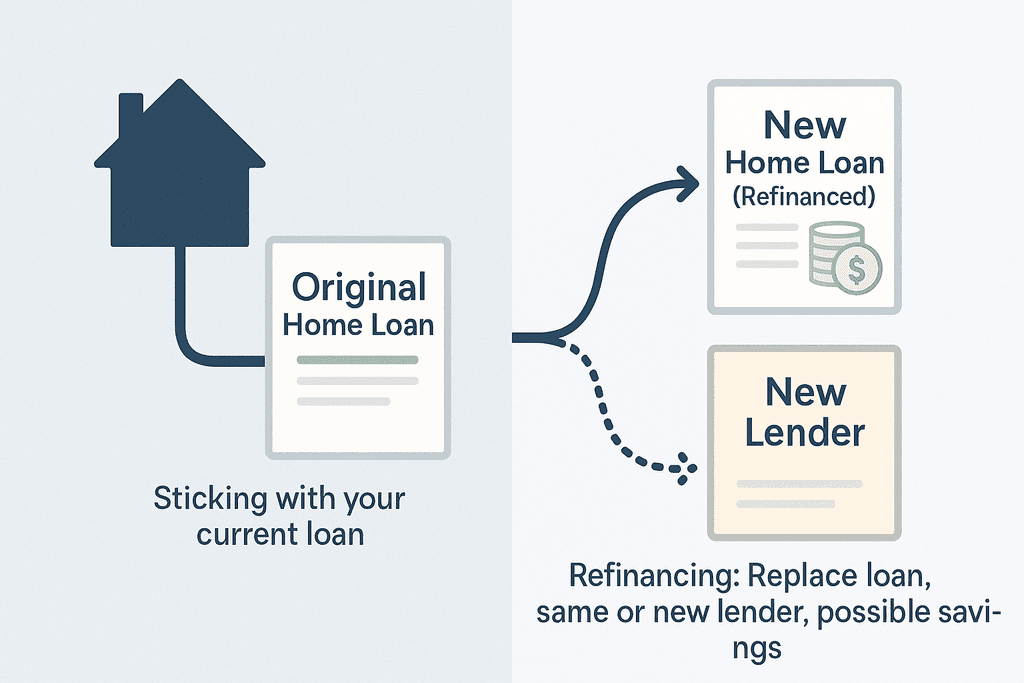

Most homeowners don’t realize they’re not stuck with their original home loan forever. Refinancing is simply the process of replacing your current home loan with a new one, either with your existing lender or by switching to a completely different bank. Think of it like trading in your old phone plan for a better deal, except this time you could save thousands of dollars every year. The basic idea is straightforward, but the details matter quite a bit when you’re dealing with something as big as your mortgage.

When you refinance, you’re essentially going through a simplified version of what you did when you first bought your home. The new lender (or your current one) will need to check a few things before approving your new loan. At Credific Finance, we handle this entire process for our clients, working with over 40 lenders to find the best fit.

Here’s what typically happens during refinancing:

The Australian property market has seen some wild swings lately, and interest rates have been on a rollercoaster. Recent rate changes have created a perfect storm for refinancing opportunities, especially for homeowners who locked in their loans a few years ago. Many Sydney residents are discovering they’re paying way more than they need to.

According to recent expert analysis, the old rule about needing a 1% rate difference to make refinancing worthwhile doesn’t always apply anymore. The math has changed, and even smaller rate differences can lead to significant savings when you factor in better loan features and reduced fees.

| Loan Amount | Old Rate | New Rate | Monthly Saving | Annual Saving |

|---|---|---|---|---|

| $500,000 | 6.5% | 5.9% | $178 | $2,136 |

| $700,000 | 6.5% | 5.9% | $249 | $2,988 |

| $900,000 | 6.5% | 5.9% | $320 | $3,840 |

You’ve got two main options when refinancing. You can stick with your current lender and negotiate better terms, or you can shop around and switch to someone new. Switching lenders often gets you access to competitive “honeymoon rates” and cash-back offers that existing customers rarely see. Banks want new business, and they’re willing to pay for it.

Staying with your current lender is usually faster and involves less paperwork. But here’s the catch – they know you’re already comfortable with them, so they might not offer their absolute best rates. That’s where working with a broker makes sense, because we can compare what your current lender offers against 40+ other options to make sure you’re actually getting the best deal available.

Most homeowners don’t realize they’re paying thousands more than they need to on their mortgage. The average Australian home loan sits untouched for years, even as market rates drop and better products emerge. If you took out your loan more than two years ago, there’s a good chance you’re overpaying right now.

Clear Signs You Should Refinance Now

The clearest signal that refinancing makes sense is when your current rate sits 0.5% or more above what’s available in the market. That might not sound like much, but on a typical Sydney mortgage, it adds up fast. Your lender isn’t going to call and offer you a better deal, even if they’re giving new customers rates well below what you’re paying.

Here are the situations where refinancing typically makes the most sense:

Property values across Sydney have shifted considerably over the past few years. If you bought during a lower market period, you might have more equity than you think. That equity opens doors to better loan products with lower rates and more flexible features.

Your circumstances matter more than market conditions alone. Maybe you were self-employed when you first bought and could only access limited loan options. Now that you have a longer trading history or more stable income documentation, lenders view you differently. The loan that made sense three years ago might be holding you back today.

Quick Assessment Checklist:

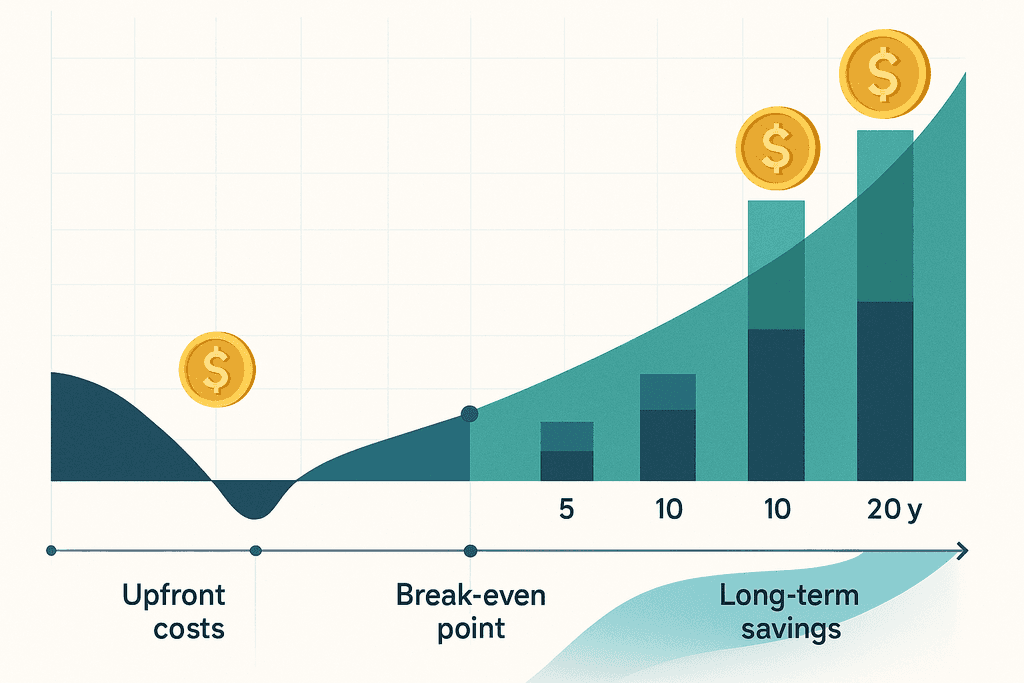

Refinancing isn’t free, and anyone who tells you otherwise isn’t being straight with you. You’ll face some upfront costs that need to be weighed against your potential savings. The good news is that for most people in the right situation, the numbers work out favorably within the first year or two.

The Real Costs and Savings Breakdown

Typical refinancing costs include application fees (usually $200-600), valuation fees (around $200-300), and discharge fees from your current lender (typically $150-400). Some lenders waive application fees as part of promotional offers, but you need to look at the total package. A loan with no application fee but a higher ongoing rate isn’t doing you any favors.

Here’s what the math actually looks like:

The break-even calculation is straightforward but crucial. Add up all your refinancing costs, then divide by your annual savings. That tells you how many months until you’re ahead. If you’re planning to stay in your property longer than that break-even period, refinancing makes financial sense.

Watch out for hidden costs that can eat into your savings. Some loans come with ongoing monthly fees that seem small but add up over time. Others offer attractive introductory rates that revert to much higher rates after a year or two. According to research on refinancing trends, understanding the full cost structure prevents surprises down the track.

The Loan Comparison Calculator we provide at Credific lets you run these numbers yourself with your actual figures. You can see exactly how different loan options stack up against your current situation, including all fees and rate differences over time.

The refinancing process sounds more complicated than it actually is when you know what to expect. Most people put it off because they imagine mountains of paperwork and endless back-and-forth with lenders. The reality is that with proper guidance, the whole thing can be wrapped up in a few weeks without taking over your life.

Start with a loan health check to understand where you stand right now. This means looking at your current rate, loan features, equity position, and how your financial situation has changed since you first borrowed. You need this baseline before you can properly evaluate whether switching makes sense.

The refinancing process follows these steps:

The documentation part trips people up, but it’s pretty standard stuff. Lenders want to see proof of income, details about your assets and liabilities, and information about the property. If you’re self-employed, the requirements get a bit more detailed, but it’s nothing that can’t be handled with the right preparation.

This is where working with a broker makes the biggest difference. At Credific, we handle the lender communications, chase up any missing information, and manage the timeline so everything happens smoothly. We’ve done this over a thousand times, so we know exactly which lenders will look favorably at your specific situation and how to present your application for the best outcome.

Required Documents Checklist:

Getting a lower interest rate is the obvious reason to refinance, but it’s far from the only one. Many people use refinancing as an opportunity to restructure their entire financial setup in ways that better serve their current goals. The right refinancing strategy can unlock opportunities that weren’t available when you first bought.

Accessing your equity is one of the most powerful reasons to refinance. If your property has increased in value or you’ve paid down your loan, that equity can fund your next investment property deposit, major renovations, or other wealth-building moves. This is called a cash-out refinance, and it lets you put your property’s value to work without selling.

Other strategic reasons to refinance include:

Debt consolidation through refinancing can be particularly effective if you’re carrying multiple high-interest debts. Financial experts note that rolling these into your home loan at a much lower rate saves money, but only if you’re disciplined about not running up those credit cards again.

For property investors, refinancing opens up sophisticated structuring options. You might want to split your loan into multiple accounts, set up interest-only payments on investment portions while paying down your home faster, or restructure to maximize tax deductions. These strategies require careful planning to get right.

Self-employed clients often find that refinancing a few years into their business gives them access to much better loan products. Once you have a solid trading history and clear financials, lenders view you more favorably. We’ve helped hundreds of self-employed borrowers restructure their loans to access better rates and features that weren’t available when they first started out.

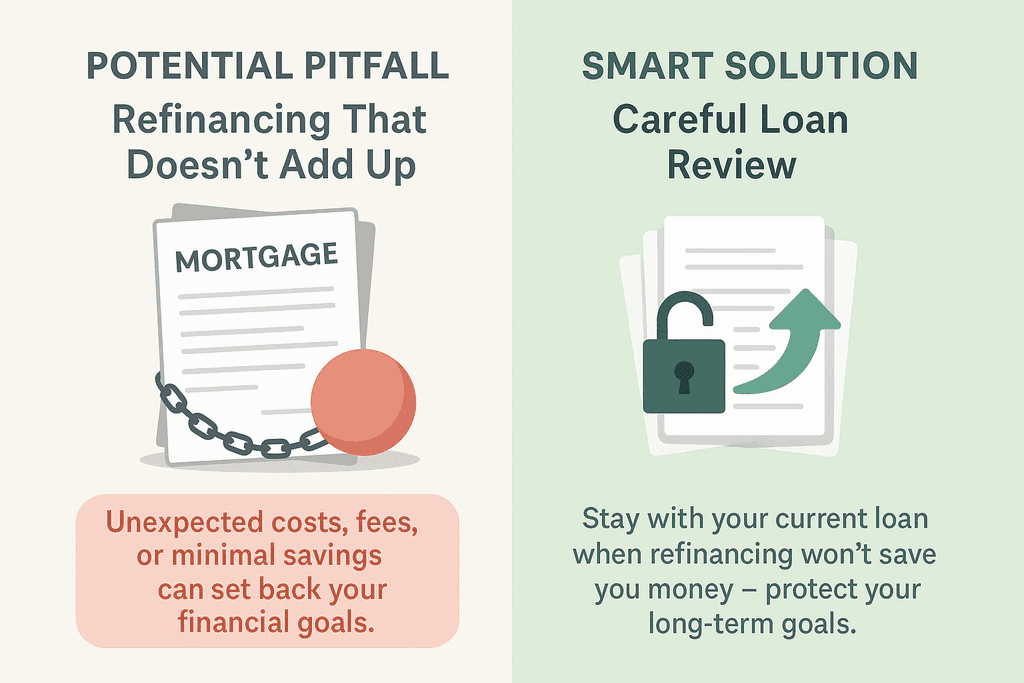

Here’s something most brokers won’t tell you upfront: refinancing isn’t always the smart move, even when rates look tempting. The mortgage industry loves to push refinancing as a universal solution, but the reality is more nuanced. Sometimes staying put with your current loan actually saves you more money in the long run. Understanding when to hold off on refinancing can protect you from making a costly mistake that sets your financial goals back by years.

If you’re close to paying off your home loan completely, refinancing rarely makes financial sense. The costs involved in switching lenders can actually extend your debt timeline unnecessarily.

Fixed rate loans come with a hidden trap that catches many borrowers off guard. Break costs can run into tens of thousands of dollars if you exit a fixed loan early, especially when market rates have dropped since you locked in.

Key Stat: Break costs on a $500,000 fixed loan can exceed $20,000 if exited 2+ years early during a falling rate environment.

Your current lender might also charge exit fees, discharge fees, and other administrative costs. At Credific Finance, we’ve seen clients who would have lost money refinancing once we calculated their specific break-even point against potential savings.

Market conditions don’t always work in your favor. If your property value has dropped since purchase, you might find yourself above the 80% loan-to-value ratio threshold.

Your financial situation matters more than you think. If you’ve changed jobs recently, become self-employed, or taken on additional debt, refinancing approval becomes significantly harder.

A 0.10% rate difference sounds appealing until you do the math. Small rate improvements often don’t justify the switching costs involved in refinancing.

Break-Even Reality: On a $400,000 loan, a 0.15% rate reduction saves just $600 annually. With $4,000 in refinancing costs, you won’t break even for nearly 7 years.

Calculate your specific break-even point by dividing total refinancing costs by your annual interest savings. If that number exceeds 3-4 years, refinancing probably isn’t worth it, especially if you’re planning to sell or upgrade soon.

Refinancing your home loan isn’t something you should rush into, but it’s also not something you should ignore. The right refinance at the right time can save you tens of thousands of dollars over the life of your loan. The wrong one can cost you money and waste your time. The key is knowing which situation you’re in, and that comes down to doing the math on your specific circumstances.

Here’s what really matters when you’re making this decision:

Most people don’t realize how much they could be saving because they’ve never actually compared their current loan against what’s available now. The market has changed a lot, even in just the past year or two. At Credific Finance, we work with over 40 lenders, which means we can show you options you probably didn’t know existed and negotiate terms that work specifically for your situation.

The easiest way to start is with a simple loan health check. You don’t need to commit to anything or fill out mountains of paperwork. Just a quick look at where you stand now versus where you could be. Our calculators can give you a rough idea in minutes, or you can reach out for a free assessment where we dig into the actual numbers that matter for your loan.

If the signs are pointing toward refinancing, the next step is understanding exactly what that process looks like and what questions you need answered before moving forward.

Refinancing can feel overwhelming when you’re not sure what to expect. These are the questions we hear most often from clients considering a switch, and the straight answers you need to make a confident decision. Whether you’re worried about timing, credit impacts, or what happens to your existing loan features, we’ve got you covered.

Most refinances take between 4 to 6 weeks from application to settlement. The timeline depends on how quickly you can gather documents, how fast your new lender processes the application, and whether your property valuation comes back without issues. At Credific Finance, we handle all the paperwork and lender communications to keep things moving smoothly, often getting clients through faster than the average timeframe.

Yes, but usually only temporarily and minimally. When you apply for refinancing, lenders perform a credit check which can cause a small dip in your score. As long as you make your repayments on time with your new loan, your score typically recovers within a few months. Avoid applying with multiple lenders at once, as each application creates a separate credit inquiry that can add up.

Absolutely, though it requires more documentation and the right lender match. Self-employed borrowers typically need to provide two years of tax returns, business financials, and sometimes additional proof of income stability. Credific Finance specializes in complex lending scenarios, including self-employed clients, and we know which lenders are most flexible with non-traditional income structures. We’ve successfully refinanced hundreds of self-employed clients who thought they’d be stuck with their current rates.

Your existing offset account will close when you pay off your old loan, but you can set up a new offset account with your new lender. The funds in your current offset simply transfer to your regular bank account, and you can move them into your new offset once it’s established. Not all loan products include offset accounts, so make sure to request this feature if it’s important to your financial strategy.

No, you don’t pay stamp duty when refinancing your existing home loan. Stamp duty only applies when you purchase property, not when you switch lenders on a property you already own. You will need to budget for other costs though, like discharge fees from your current lender, application fees with the new lender, and potentially valuation fees.

It’s possible, but it depends on how much equity you have left. If your property value has dropped and you now have less than 20% equity, you might need to pay lenders mortgage insurance or look for lenders who accept higher loan-to-value ratios. Some lenders are more flexible than others in these situations, which is where working with a broker who has access to 40+ lenders makes a real difference in finding an option that works.

📞 Contact Credific Finance today to explore your refinance home loan options and take control of your financial future!